GXBank Malaysia Review: Should You Make The Switch?

GXBank Malaysia Review: In-depth analysis of Malaysia's first digital bank covering its digital features, user experience, and potential benefits for customers.

The wait is finally over!

Malaysia’s first digital bank, GXBank by Grab, is now available to the public. It’s such a big deal that in less than two weeks, it has managed to rack up over 100,000 users.

But is the hype a fab or simply a fad? And should you make the switch over? Well, here’s my first impression and review of GXBank Malaysia.

Getting To Know GXBank by Grab

GXBank is Malaysia’s first digital bank and among the five successful digital bank licence applicants approved by Bank Negara Malaysia (BNM). It is a subsidiary of Singapore’s GXS Bank – a joint venture between Grab and Singtel, along with a consortium of other Malaysian investors, including the Kuok Group.

As a licensed bank by BNM and a member of Perbadanan Insurans Deposit Malayisa (PIDM), deposits up to RM250,000 are protected by PIDM per user.

Prior to their launch, a beta test was conducted in September this year, where 20,000 early users provided feedback to improve the platform including creating ‘Pockets’ – the app’s savings goal feature.

What Sets GXBank Apart From Traditional Banks (Maybank, CIMB, RHB, etc)?

Well, some of its unique features include:

#1 Being fully digital

Kind of a no-brainer, this digital bank exists fully on their app. Other than their main office, GXBank will not have any physical bank branches nor ATMs.

Now, this may raise some concerns. How will users withdraw physical cash? What if you’re facing issues with your account and there are no counter/bank branches you can visit?

Let’s address the issue of withdrawing physical cash first. According to GXBank chief executive, they will be introducing a debit card sometime in January 2024 where users will be able to use every ATM connected to the MEPS shared ATM network to withdraw money from. Best part is, GXBank said they will waive the RM1 surcharge you’ll get when you use other bank’s ATMs.

Now for the issue of having no physical counters/banks, if users are faced with a problem regarding their account, they can simply reach out to GXBank, 24/7 through online means. The banking platform has set up an in-app live chat, customer service hotline, and support email to ease user-provider communications.

So, everything from opening an account to any transactions will all be fully digital.

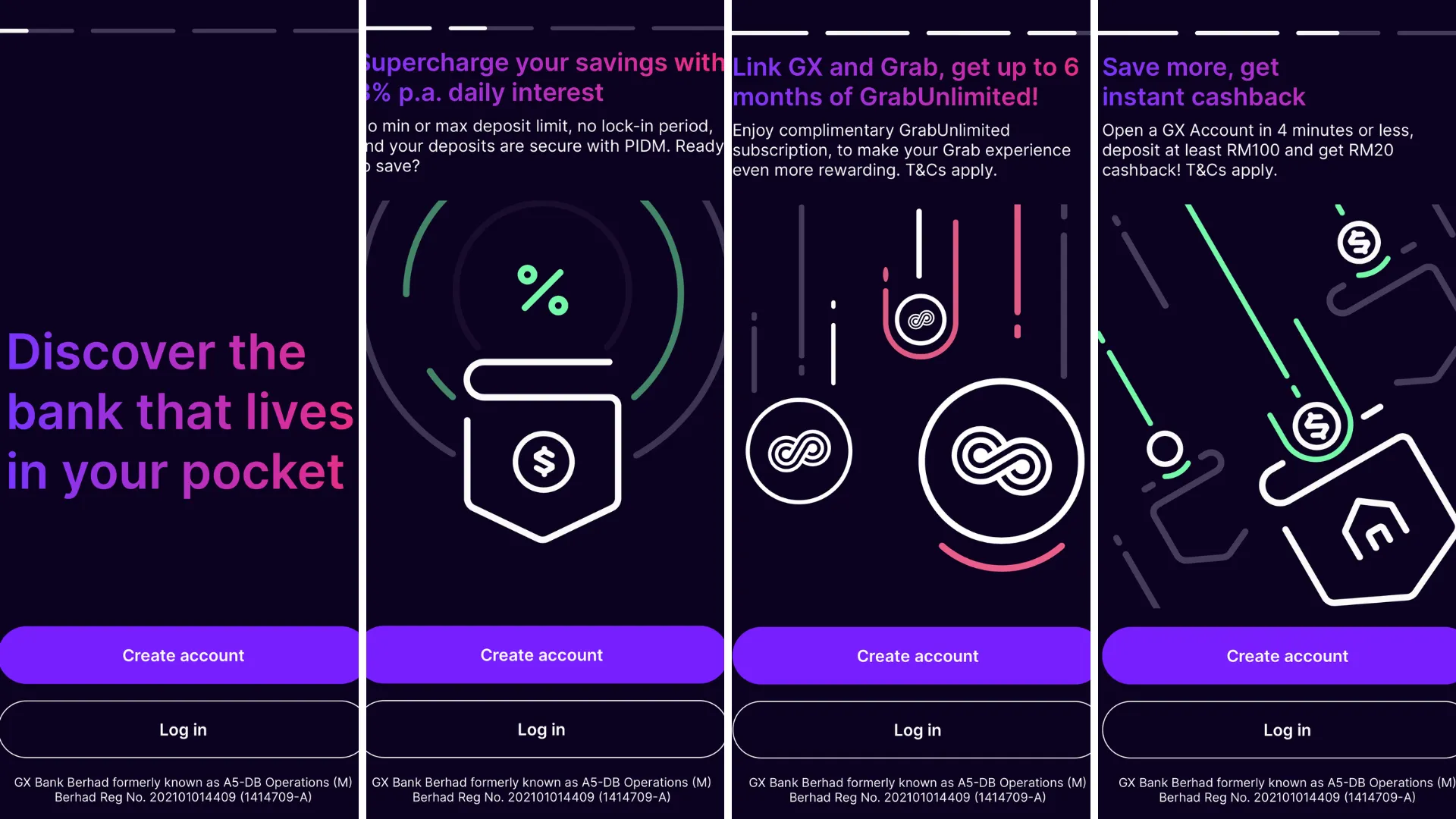

#2 Savings Account with 2% p.a. daily interest

This is definitely one of their most attractive features – a savings account that accrues daily interest of 2% p.a. with a pretty low deposit. Think Touch n’ Go GO+ account, it works the same way.

GXBank will deposit the daily interest into users’ accounts if it’s at least RM0.01. With that in mind, the minimum you’ll need to start earning its daily interest is RM60.84. In comparison to traditional banks, most will require you to have a relatively high available balance to earn any sort of interest. Even then, the interest rate is quite low at < 2.5% p.a.

Its savings account will also have no minimum balance and lock-in periods required.

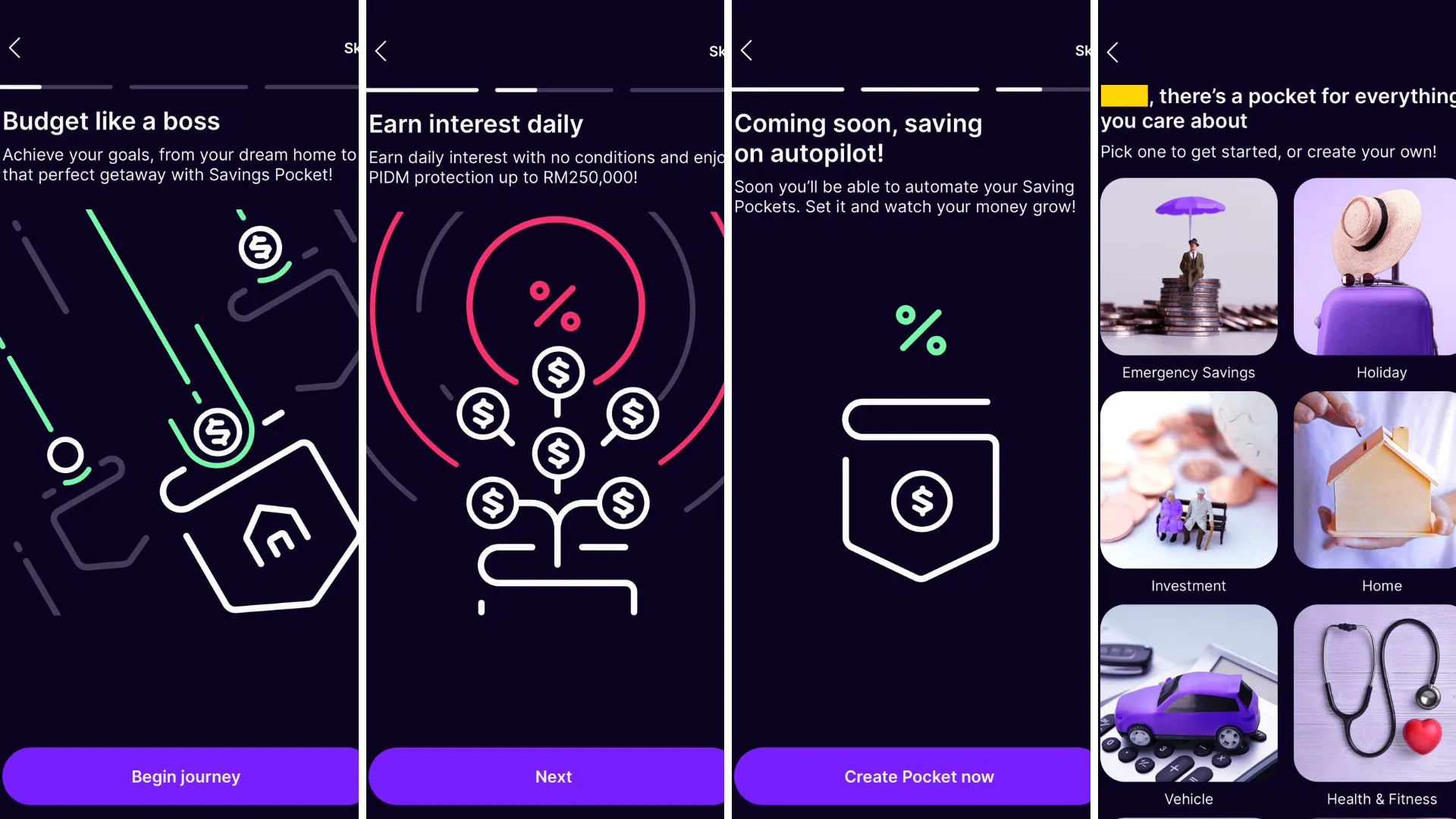

#3 ‘Pockets’ feature to encourage savings

As suggested by their beta testers, GXBank has a ‘Pockets’ feature that encourages goal-intended savings. And just like its savings account, users will be able to enjoy the same 2% p.a daily interest.

So, whether you want to start an emergency fund or a vacation sinking fund, you can do it with ‘Pockets’. Currently, MAE by Maybank also has a savings feature – ‘Tabung’ but what sets GXBank’s ‘Pockets’ apart is the potential to earn daily interest.

#4 GXBank debit card with unlimited 1% cashback

As previously mentioned, GXBank is planning to introduce a debit card in January 2024. Just like any other debit card, you can use it to spend and withdraw money.

However, what makes GXBank’s soon-to-launch debit card so cool is that users will be able to earn unlimited 1% cashback every time they pay for something.

Technically, this means you could potentially untung 4% in interest/savings simply by using GXBank (if you were to get the debit card).

#5 Zero fees!

Whether it is ATM withdrawals, intrabank funds/DuitNow transfers or even foreign currency exchange transfers, GXBank will not be charging any fees.

Say goodbye to hidden chargers and sneaky fees!

#6 Seamless GXBank-Grab ecosystem

These days, living within the same ecosystem makes everything more convenient and seamless. Think about it: if you’re a die-hard Apple user, the likelihood is that you’ll want (or maybe already have) more than one Apple device. You can just AirDrop files or get Siri to do things for you!

With GXBank and Grab, it’s the same thing – you’ll be living within one ecosystem. So, if you’re a heavy Grab user, switching over to GXBank may just make everything so much smoother! Of course, the most obvious perk would be earning more GrabReward points.

BTW, if you were to open a GXBank account now, you’ll get to enjoy some awesome deals including:

-

RM20 cashback when you deposit RM100 or more.

-

RM8 instant cashback when you link your DuitNow to GXBank.

-

Up to 6x GrabUnlimited subscriptions worth RM29.40 (RM4.90/month x 6).

My Review of GXBank Malaysia

GXBank: Account opening

I’ve read some articles of people saying it takes them longer than the advertised 4 minutes to open an account but for me, it really only took more or less 4 minutes to do it.

It was super fast and the process was already one I was familiar with – the standard finance/investment app account opening including eKYC, personal details, OTP, contact information, employment details, tax residency, as well as declarations and agreement.

GXBank: Account funding

Since it’s a digital bank, I can’t go to any counters to bank in my initial deposit. Then that leaves me with either transferring funds from my existing (traditional) bank account or making my GXBank account the bank account for my salary to come into. I opted for the first option. Also, I wouldn’t advise any of you to make your GXBank account your “salary account” cause it’s still too premature for that (explained more later).

Anyway, I deposited RM100 into my GXBank account to get the RM20 cashback (which I got instantly). This process follows the standard FPX payment.

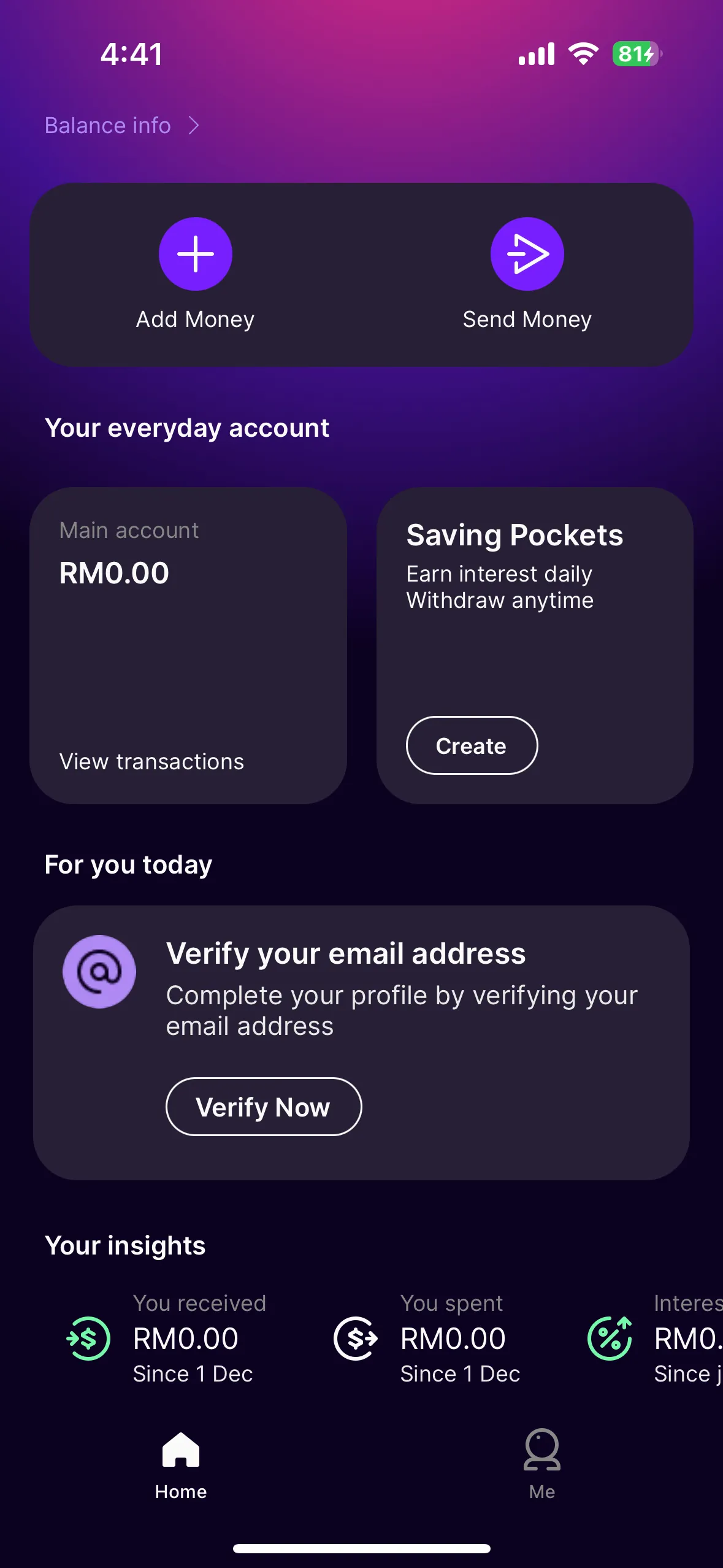

GXBank: Account functionality

At the time of this article, there are only three features available – Add Money, Send Money and Saving Pockets. I can also get Insights like Fund Received, Funds Spent and Interest Earned.

Honestly, for now, I’m not impressed. I can’t pay for anything cause there’s no DuitNow QR code feature. So, I can’t scan or even show my QR code. I suppose the point is to use my Grab app’s QR code but even then, I have a problem with it and this leads me to my next point.

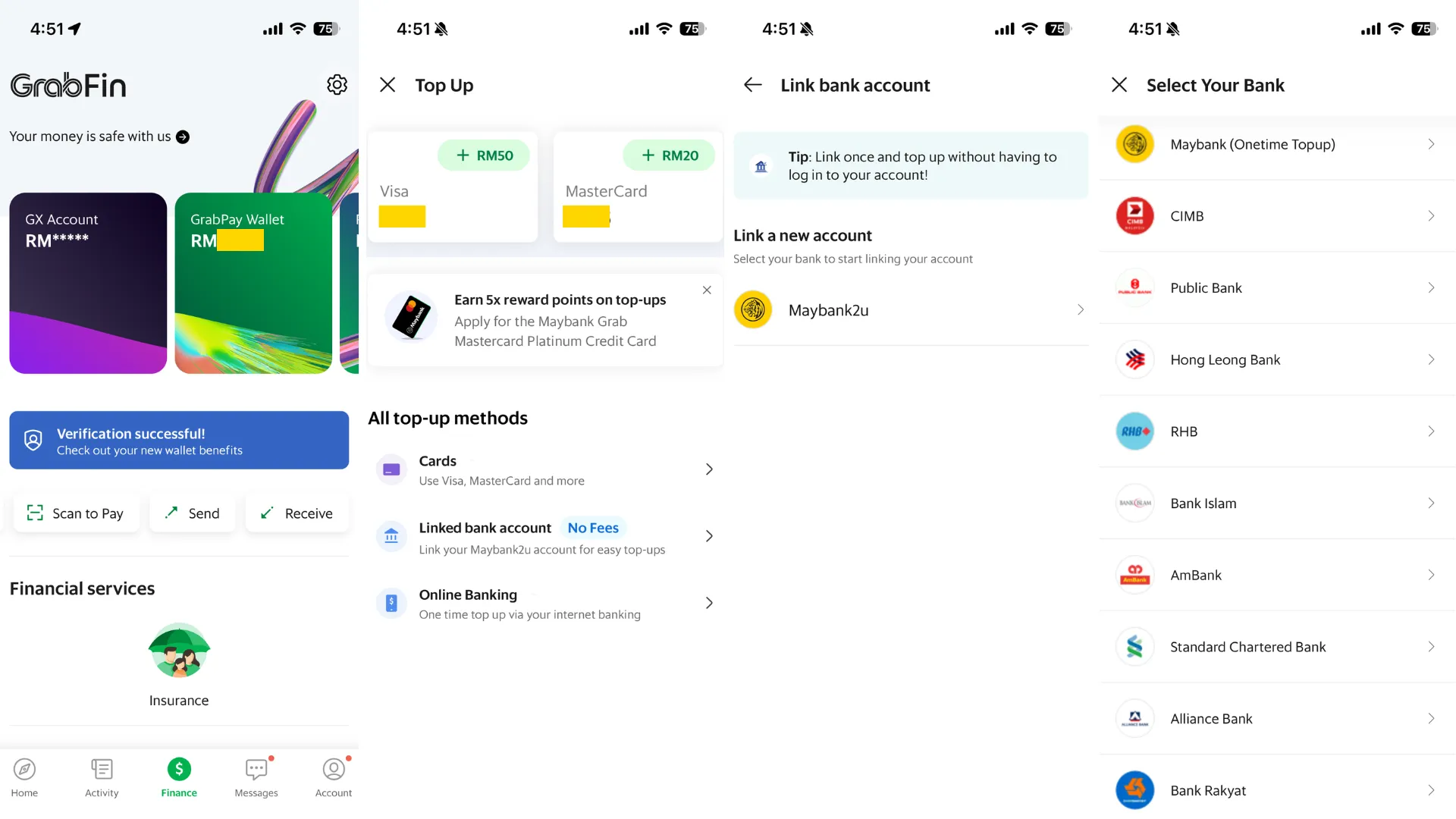

GXBank: Not very “seamless” GXBank-Grab ecosystem

One of the reasons I opened a GXBank account this early on is because I thought I’d be able to benefit from the GXBank-Grab ecosystem. Alas, that wasn’t the case.

I’ve already linked my GXBank account to my Grab account but for some reason, I can’t figure out how to fund my GrabPay Wallet using GXBank.

Not sure if it’s just a glitch on my end but there’s no option to fund my GrabPay Wallet using GXBank. I’m still using my existing and previously linked bank accounts to fund my Wallet. Perhaps, you guys can let me know if it’s the same for you? Reach out to me on Instagram, I would love to hear from you.

GXBank: App design

Just like the Grab app, the GXBank app design is very clean and straightforward. Everything is just a touch away and the UI/UX is super intuitive.

If you’re already familiar with other financial/investment apps like MAE or M+ Global, you’ll have no problem adapting to the GXBank app.

Should You Make The Switch To GXBank?

Personally, I think it’s still too premature for that. GXBank is still in its infancy so they’re still in their early days.

The only incentive to switch over now is the deals you get and the accruement of daily interest – even then, Touch n’ Go GO+ is offering higher interest at 3.56% p.a.

Perhaps when more features come out and their debit card is rolled out, then you can consider opening an account. Either way, I’m already on it and I don’t regret it lah.

I’m excited to see how GXBank and the overall digital banking industry will evolve in the future. Maybe there will come a time when we’ll be able to apply for car/house/personal loans, credit cards or even insurance through these revolutionary apps.

Subscribe to our financial newsletter for the latest news, insights, and advice on personal finance, investing, and more. With every email, you’ll gather the confidence and knowledge to make informed decisions to achieve your financial goals.